CASE STUDY // BANKING // BUILD / ADVISE

Credit Intelligence.

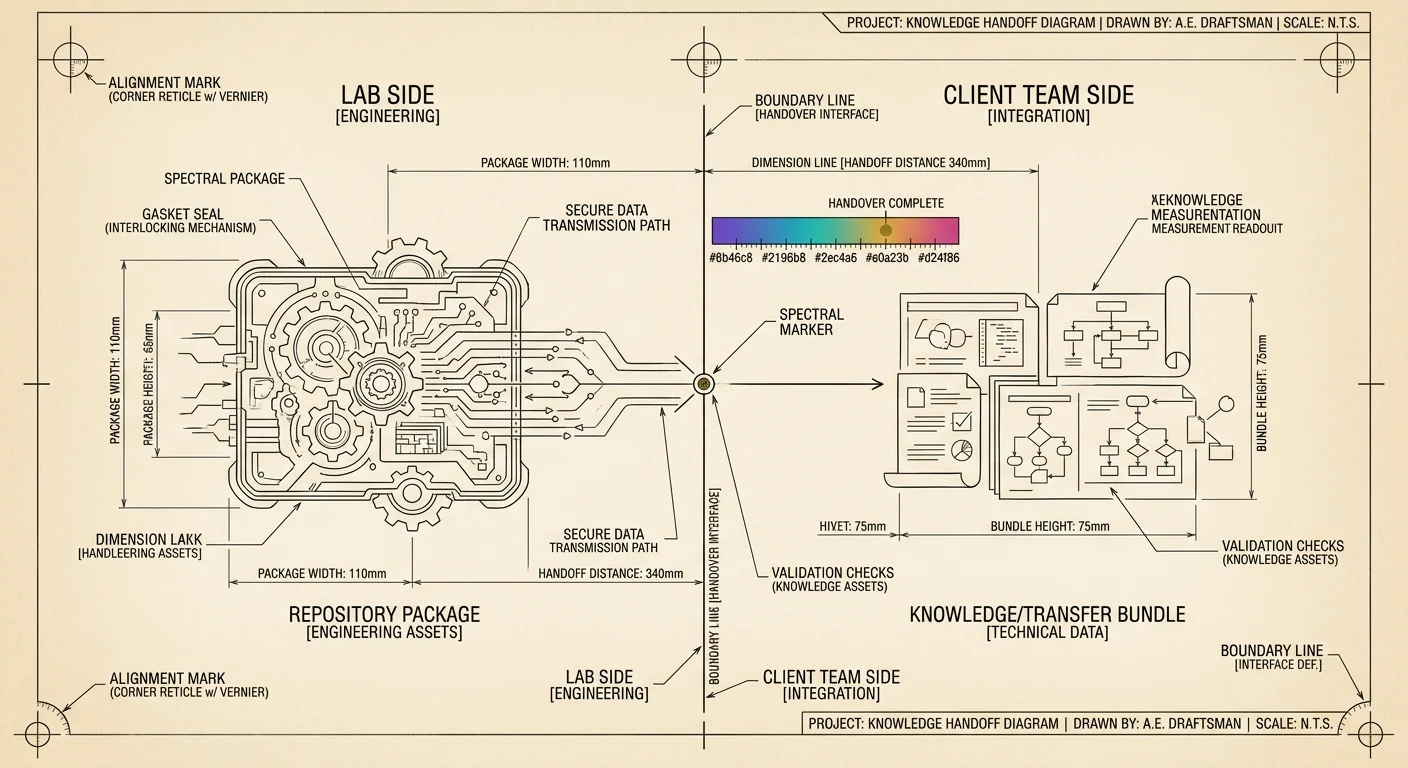

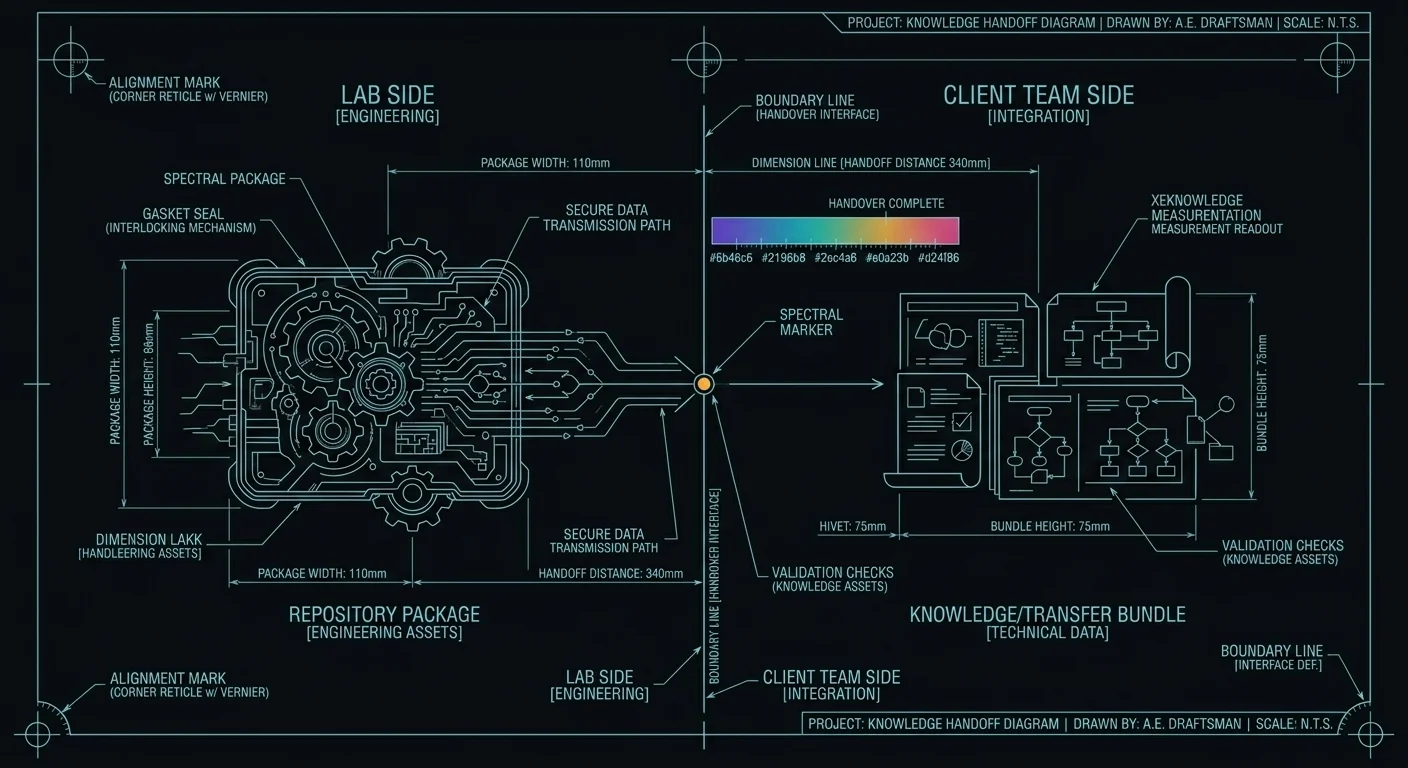

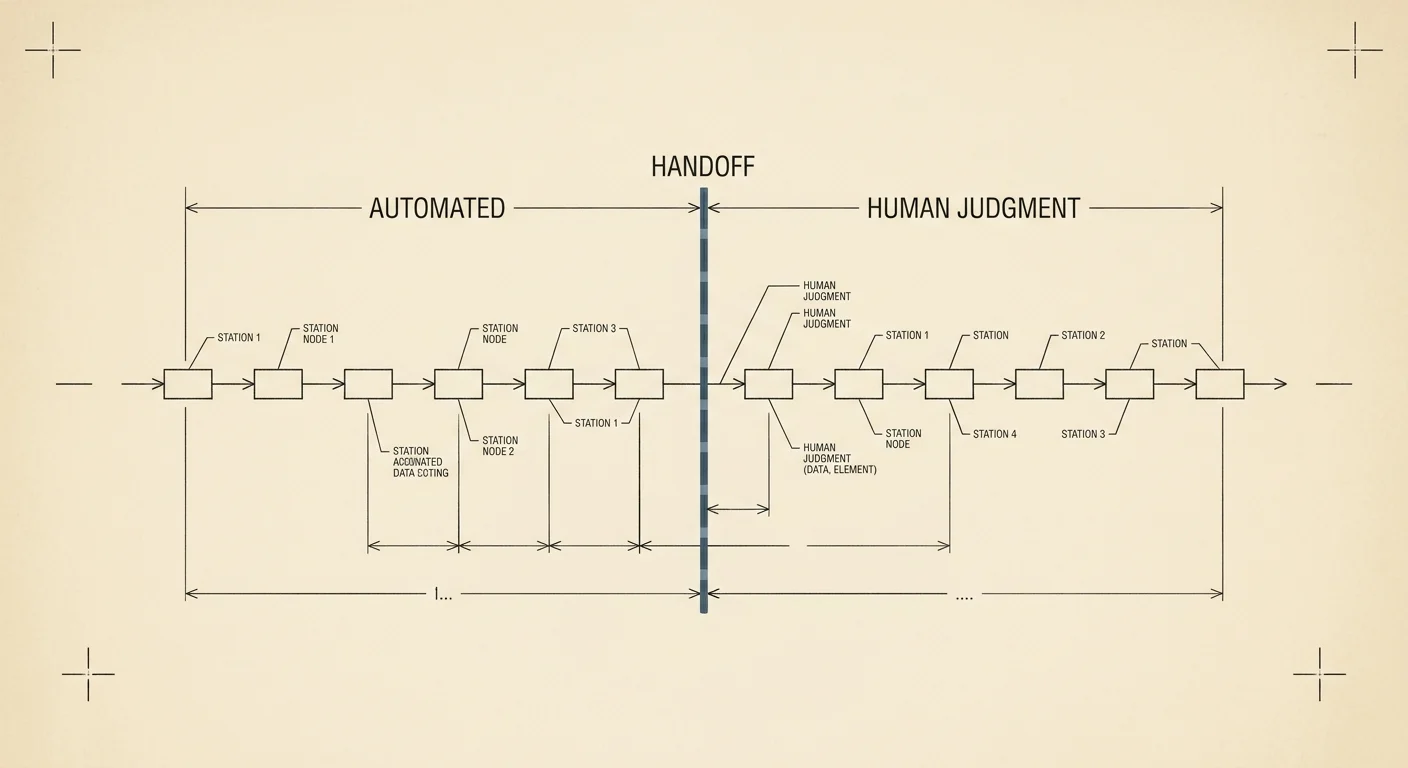

A top-tier US private and commercial bank wanted to grow its loan book substantially without growing headcount in proportion. We built a credit-intelligence layer that drafts the twenty-two sections of a Credit Approval Memo from systems of record and checks executed loan terms against what was approved — extending the bank's process, never replacing it.

The work was about knowing which knob to turn: automate the assembly, leave the judgment human, and draw that line in the data model rather than the interface.

SPEC_ID: WORK-01 // CAPABILITY: BUILD + ADVISE // SECTOR: BANKING

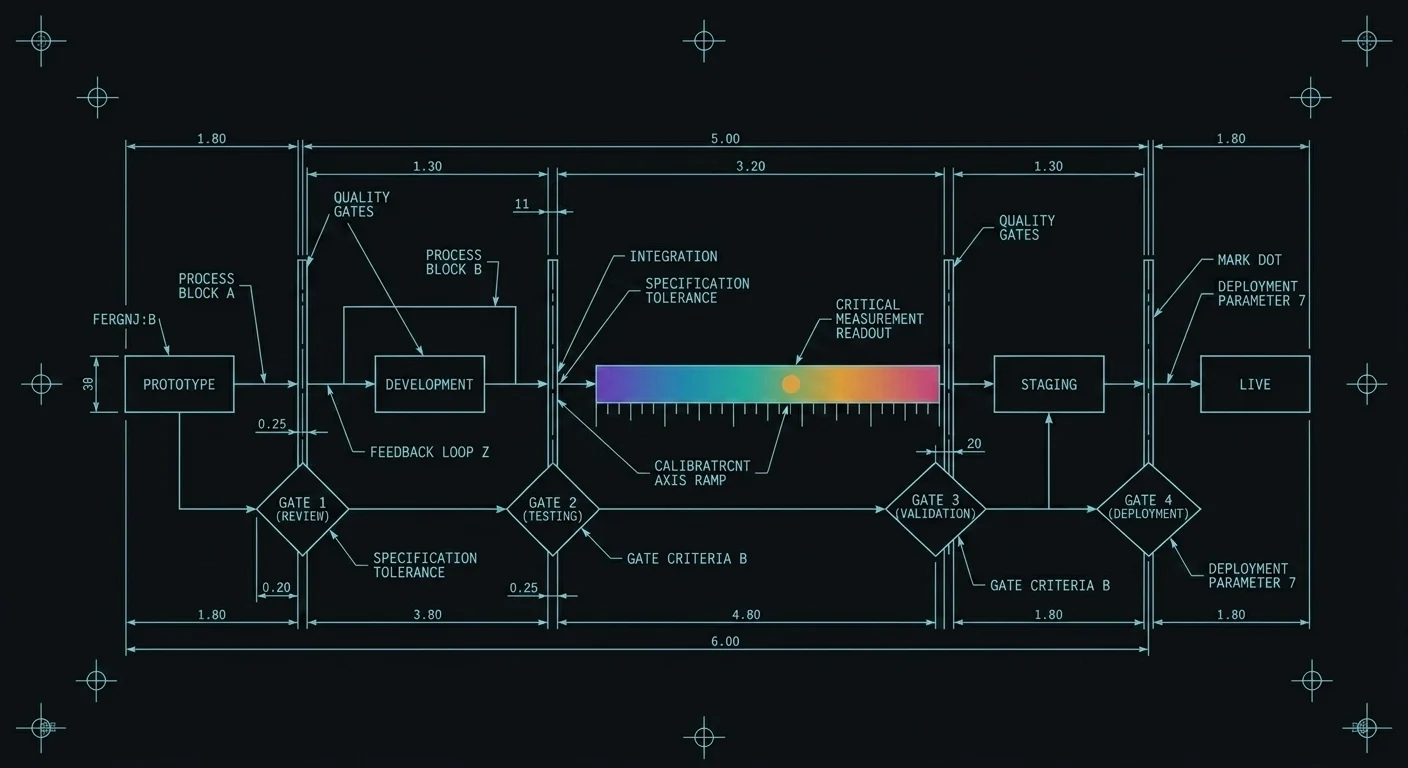

FIG. ASSEMBLY → JUDGMENT HANDOFF

REF: CI-00